What is Lifetime Income?

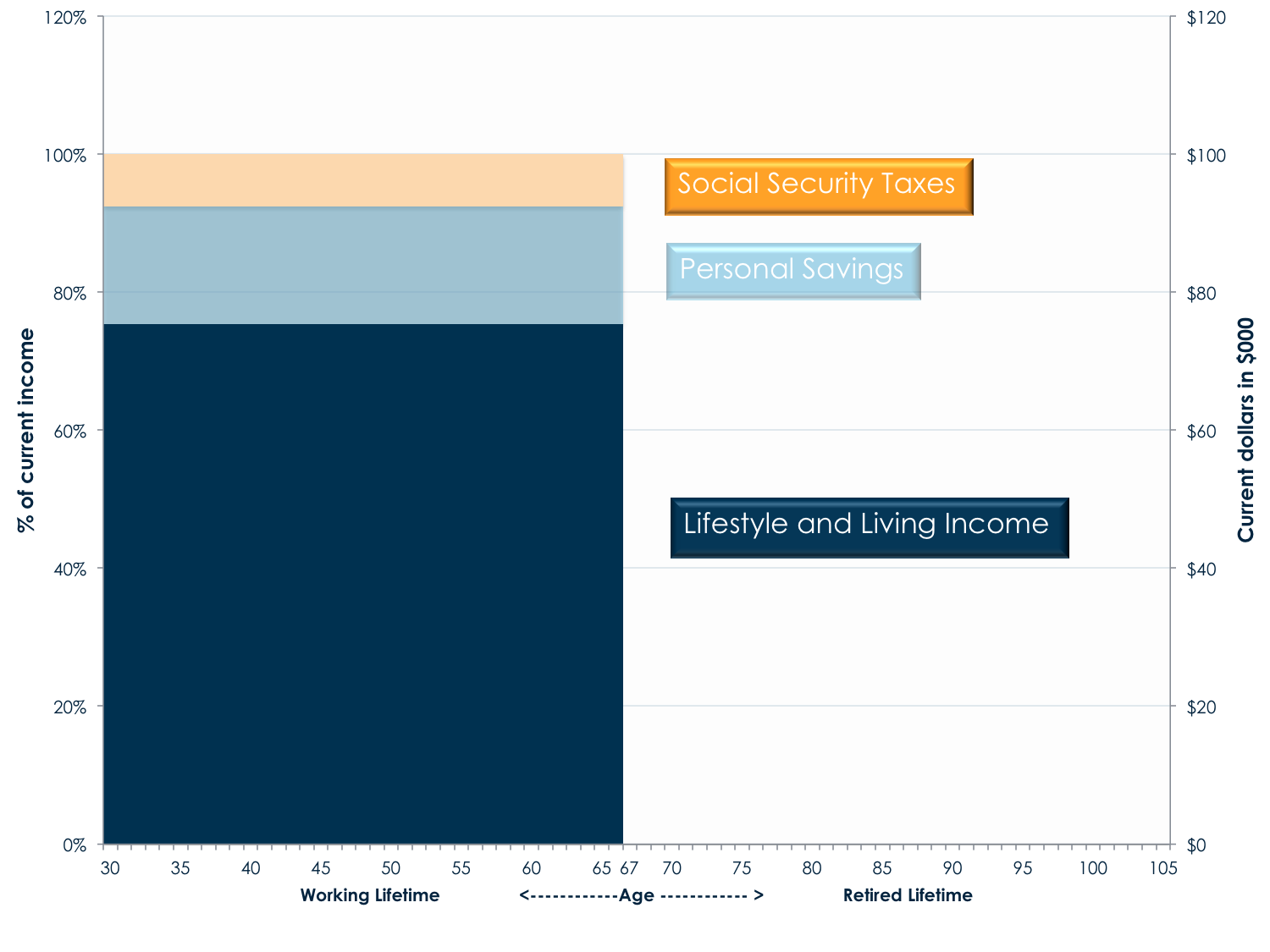

Your total lifetime can be divided into two parts: a working lifetime and a retired lifetime. What you earn during your working lifetime needs to provide you with enough income (in combination with Social Security and any employer-provided savings or income) to last over your total lifetime.

Try our lifetime income estimator to get an idea of the balance that's right for you. Contact us if you'd like to know more.

Working Lifetime

While you are working, you pay Social Security Taxes (a form of retirement saving), and you are saving additional amounts (hopefully!) to secure your financial future.

The remainder of your income provides for your lifestyle and living expenses, including income taxes. This is often called your "standard of living."

Retired Lifetime

In retirement, your sources of income include Social Security, an employer pension (if you are lucky enough to have one), assets provided by employer contributions to a 401(k) or 403(b) plan, and your own assets and future savings.

Although not shown on the chart, you may also have part-time work to supplement your retirement income. This could (and should!) be factored into the analysis.

Balancing

The two variables that are most within your control are how much you save when you are working, and when you expect to retire.

Saving has two beneficial effects: First, it means that you're adjusting your lifestyle and living expenses to a lower level of income. Second, it provides more money to spend during your retired lifetime.

Likewise a later retirement date has two beneficial effects: First, it gives you more time to accumulate money for retirement. Second, it reduces the length of time over which you have to spread your retirement assets, making more money available each year. Part-time earnings in retirement (not shown) can also help reduce the need for income from other sources.

Being on track to meet your future financial goals starts with finding the balance between current and future lifestyle choices that's right for you. A good initial starting point is to aim for a level of post-retirement income that's consistent with your pre-retirement lifestyle and living expenses. This amount provides planning flexibility and a cushion against higher than expected expenses — either before or after retirement — or earlier than expected retirement.

A less conservative approach with less cushion and long term flexibility would follow research that suggests that average spending needs may decline by 1.7% - 2.4% per year in retirement.